If you’ve ever told yourself “I’ll save whatever is left at the end of the month,” you already know it rarely works. This guide shows you how to calculate monthly savings goals in a clear, structured way — so you stop guessing and start planning with numbers.

Whether you’re saving for an emergency fund, vacation, house down payment, or retirement, this method gives you a realistic monthly target.

Quick Answer

To calculate your monthly savings goal:

Monthly Savings Needed = Target Amount ÷ Number of Months

Example:

If you want to save $12,000 in 24 months:

$12,000 ÷ 24 = $500 per month

If your savings earn interest, your required monthly amount may be slightly lower due to compound growth.

What Is a Monthly Savings Goal?

A monthly savings goal is the fixed amount you commit to saving each month to reach a specific financial target within a set time.

Instead of saving randomly, you:

- Choose a target amount

- Set a timeline

- Calculate the exact monthly contribution needed

This approach makes saving measurable and predictable.

Why Guessing Your Budget Usually Fails

People often struggle to save because they:

- Don’t track fixed expenses

- Underestimate small recurring costs

- Set unrealistic savings targets

- Spend emotionally during high-stress months

A structured calculation removes guesswork and replaces it with a clear monthly number.

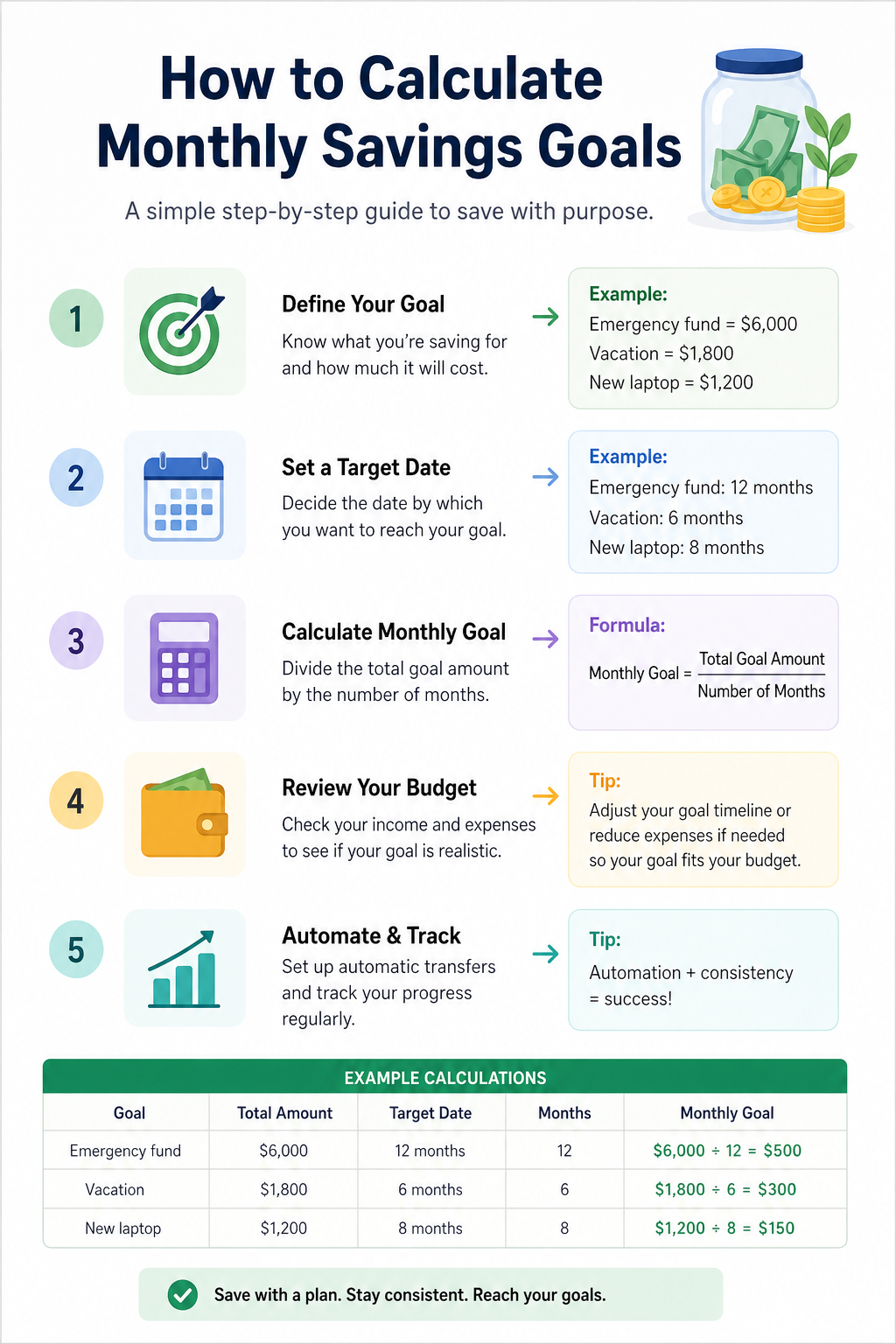

Step-by-Step: How to Calculate Monthly Savings Goals

Step 1: Identify Your Financial Goal

Examples:

- Emergency fund: $6,000

- Vacation: $3,600

- House down payment: $40,000

- Car fund: $15,000

Be specific. “Save more” is not a measurable goal.

Step 2: Set a Target Amount

Decide the exact number you want to reach.

Example:

Goal = $10,000

If you already have savings, subtract that from your goal.

Example:

Goal = $10,000

Current savings = $2,000

Remaining target = $8,000

Step 3: Choose a Timeline

How long do you have?

Example:

20 months

Be realistic. Shorter timelines mean higher monthly savings.

Step 4: Apply the Formula

Monthly Savings Goal = Target Amount ÷ Number of Months

Example:

$10,000 ÷ 20 months = $500 per month

If you’re starting with existing savings, divide only the remaining amount.

Step 5: Adjust for Interest (Optional)

If your savings account earns interest:

You can use a savings calculator to estimate how compound growth reduces the monthly amount needed.

Interest formula reference:

A = P(1 + r/n)^(nt)

Where:

- A = Final amount

- P = Principal

- r = Interest rate

- n = Compounding frequency

- t = Time in years

For short-term goals, interest may have limited impact. For long-term goals, compounding matters more.

Practical Examples

Emergency Fund

Goal: $5,000

Timeline: 10 months

Monthly savings = $500

Vacation Planning

Goal: $3,600

Timeline: 12 months

Monthly savings = $300

New Car Fund

Goal: $15,000

Timeline: 30 months

Monthly savings = $500

House Down Payment

Goal: $50,000

Timeline: 5 years (60 months)

$50,000 ÷ 60 = $833 per month

Expert Strategies to Make Your Goal Realistic

Start With Your Net Income, Not Gross

Always calculate savings from take-home pay.

If you earn $4,000 before taxes but bring home $3,000, your savings goal must be based on $3,000.

Use the 50/30/20 Framework as a Baseline

Many people follow:

- 50% Needs

- 30% Wants

- 20% Savings

If 20% of your income is lower than your target savings number, you may need to:

- Extend your timeline

- Reduce discretionary spending

- Increase income

Account for Irregular Income

If you’re a freelancer or gig worker:

- Calculate your average income over 6–12 months

- Save more during high-income months

- Build flexibility into your timeline

Consistency matters more than perfection.

Don’t Ignore Inflation for Long-Term Goals

For goals longer than 5 years:

Inflation reduces purchasing power.

A $40,000 down payment today may need to be higher in several years. Review long-term goals annually.

Common Savings Mistakes

- Setting aggressive targets you can’t sustain

- Forgetting annual expenses (insurance, holidays)

- Using credit cards while trying to save

- Not automating transfers

- Dipping into savings early

A realistic plan increases the chance of long-term success.

When This Calculation Is Enough

This simple method works well for:

- Emergency funds

- Travel savings

- Short- to medium-term goals

- Basic retirement planning estimates

For complex financial planning involving investments, tax strategies, or retirement accounts, consider speaking with a financial advisor.

What This Calculator Cannot Fully Determine

A monthly savings goal calculator does not:

- Predict market returns

- Guarantee interest rates

- Account automatically for taxes on earnings

- Adjust for inflation unless manually considered

- Replace professional financial planning

It provides structured estimates based on your inputs.

Strong Disclaimer

This guide and any related calculator provide estimates based on basic financial formulas and the assumptions you enter. Actual results may vary due to changing income, interest rates, inflation, taxes, market performance, and personal spending behavior.

This content is for general educational purposes only and should not replace advice from a qualified financial professional. For major financial decisions, retirement planning, or investment strategies, consider consulting a licensed advisor.

Frequently Asked Questions

How do I calculate monthly savings goals?

Divide your total savings target by the number of months you have to reach it. Adjust for interest if applicable.

What is a realistic monthly savings goal?

It depends on your income and expenses. Many aim for 15–20% of take-home pay, but this varies by situation.

Can I save with a low income?

Yes. Even small consistent savings build momentum. Extending your timeline can make goals manageable.

Should I include interest in my calculation?

For short-term goals, it may not significantly change your plan. For long-term goals, compounding becomes more important.

What if I can’t meet the required monthly amount?

You can adjust your timeline, reduce expenses, increase income, or revise your target amount.

Author Note

Created by the My Calcly tools team to provide clear, practical, and easy-to-use financial planning tools for everyday users.

Ready to Set Your Monthly Savings Goal?

Use our savings calculator above to enter your target amount and timeline — and get a realistic monthly savings number